Okay, it is only new to me - some Moron might call it a certified pre-owned vehicle. This monstrosity is a 1997 Chevy Suburban, perhaps the only car smaller than the Hummer and the now defunct Ford Excursion.

It gets 12 miles per gallon and currently costs $120 to fill up the out-sized gas tank.

Devil's Advocate: Do you think gasoline prices are going to plummet or something?

Not necessarily. But bear in mind I procured the car from my munificent mother-in-law. So however much I get gouged on gasoline will be offset by my purchase price of zero. Remember that gasoline is but just one cost of car ownership. It makes no sense to pay up $10,000 for a so-called fuel efficient car that will only save you $6,000 in gas. This is the subject of a recent column titled The Real Cost of Driving where the author concludes that given all of the costs, his guzzling 1992 Cadillac costs 70 cents per mile, while the green hybrid Toyota Prius will run you $1.42 a mile.

Anyway, as for my new/old Suburban, my wife will drive it 3.5 miles total per day, one round trip to the commuter rail station and for only four days a week, since she telecommutes on Fridays. Now I will be sure to take some flack for driving such a massive Earth-heater, given the preponderance of enviro-fanatics up here in Boston. I have pointed out the ironies, hypocrisies, and inanities of their cause more than sufficently. But while I was typing this up, I realized that I have probably consumed less fossil fuel than anyone I know. (Okay, my uncle, a 30 year resident of Brooklyn Heights likely consumes less than me BUT he heats the Earth with his logorrheic monologues.)

I lived car-less for nine years in Philly, walking to work and riding public transit. In New York, I took the subway a whopping one stop from Brooklyn Heights to Wall Street. And in Charlotte and Boston I have been working from home. The same goes for my wife. She also walked in Philly, subway-ed in NYC, walked four blocks to work in Charlotte, and now takes the commuter rail in Boston.

So the next time one of my mindless acquaintances make a crack about my "SUVs", I am going to make them compare 10 year energy consumption records. By the way, my wife and I now refer to our 14 mpg Ford Explorer as our "little fuel efficent car".

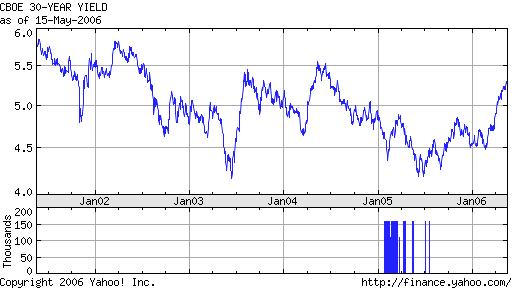

The stock market got whacked last week and I’ll explain why.

It’s because long term interest rates are rising. The econo-illiterates in the media all concur that it’s because the Fed raised short-term rates – but that isn’t really true.

First of all, the Fed only controls short-term rates. They have absolutely no control over longer term rates, the only ones that matter. The 10-year and 30-year Treasury bonds are what matter for businesses and mortgages and those yields are determined by global trading markets.

Devil’s Advocate: But everybody assumes the Fed controls all interest rates… If they can’t control longer term rates, then why did the 10 year and 30 year bonds tick up after the short term hike this week?

I think they were going to go up anyway. But this is what you see time and time again, people trying to explain security price fluctuations based on a current news cycle. My first boss (who made millions trading) told me 10 years ago that,

“...their job is to explain stock price movements...if they can’t explain it, then they won’t have a job...”

Why then the market sell-off?

First of all, when interest rates rise, bond markets attract capital away from equity markets. Every tiny .1 percentage increase in bond yields (of all durations) entices more money into T-Bills, money markets, corporate bonds, and what not. As I have noted before, I am loaded up on cash because I forecasted this rise in rates. Also note that every upward tick in yields sucks money out of real estate as well.

The market I believe is frustrated with the Fed. If the Fed wanted to slow the economy down, it should have been selling 30-year bonds in massive quantities. Selling bonds would suck cash out of the economy and would raise longer term yields and achieve their macro objective of cooling the economy. Instead, the Fed thinks that by manipulating nominal short term rates, that it can effect its goal. Not only does the Fed have this misguided notion, so does 99% of the country (if they have an opinion at all).

Let’s backtrack. The bull market of the late 1990s provided our government with budget surpluses and coincident arrogance. Emboldened by the extra money, Big Government decided they didn’t need to issue 30-year bonds any more, ceasing issuance in October 2001. This may be one of the dumbest moves ever committed by our econo-illiterate politicians. There were two major consequences.

1) With the supply of 30-year bonds cut off, the price of said bonds skyrocketed. When bond prices rise, remember their yields crater. The past five years have seen 30-year yields fall from around 6% to a ridiculous low of 4.25% in May of 2005.

Consider that there were investors locking in money for 3 decades only one year ago at 4.25%, a yield that Joe Blow gets in his money market account today. (Last May/June was also the top of the real estate frenzy – no surprise there.)

As a rule, low long term rates sow the seeds of inflation. It’s a fact that just nobody knows or cares to think about – especially not your Federal Government.

So, the Fed, by ceasing to issue 30 year bonds, actually incubated the inflation that it now seeks to eradicate.

2) Furthermore, by ceasing issuance of the 30 year bond, our incompetent Big Government was unable to take advantage of 46-year-low rates. We have minimally 100 years worth of debt obligations, but could only float bonds at these cheap rates for 10 years into the future. It took 4.5 years until the Gov’t saw its folly - 30-year bonds just resumed issuance. And there’s really no surprise that today its yield is a full point (6.25%) above last year’s low. So after almost 5 years of not borrowing against our long term obligations, the deficit is necessarily worse off than it would be otherwise AND it’s costing more to finance.

Devil’s Advocate – But didn’t the suspension of the 30 year bond cause the plummet in interest rates?

It played a role for sure. Yields may not have fallen as far as 4.25%, but they were in a major downtrend already. Anyway, so long our government is promising cradle-to-grave entitlements and doling out hundreds of millions each time a typhoon hits a banana republic, it has no business spending money that not only it doesn’t have, but doesn’t feel compelled to borrow.

It's precisely malfeasance like this that gives rise to goldbugs and other conspiracy theorists. Many goldbugs think the government secretly is trying to cause inflation and dollar depreciation in order to devalue the national debt. Many others are convinced that the dollar will soon be worthless and that the government has sold all of the gold in Fort Knox and other Reserve Banks.

With today's $700 an ounce gold price and equity weakness, the markets are definitely saying something.

I believe they're simply saying we have some commodity inflation and the Federal Reserve is powerless to do anything about it. All we can hope for is that the government doesn't exacerbate the problem it helped create.

This is a fashionable sign in my neighborhood these days. Some politician (John Tobin) is disseminating them in hopes of effecting safer driving.

First of all, I am all for safer driving. The riskiest thing Americans will ever do is travel by car. Over seven hundred people a week die in car accidents - that adds up to over 40,000 last year alone. It's just tougher to blame these deaths on George Bush, so the media sticks to exaggerating the relatively inconsequential deaths in Iraq.

Most people are safe drivers; there are however a minority out there that endangers lives just about every time they get behind the wheel. Anyone who thinks that signs are going to persuade self-centered bastards to drive more carefully is hopelessly naive. What they need on the roads is stricter traffic law enforcement - not front lawn suggestions.

Though again, this is Boston. This is how they do things up here. There might not be a greater concentration of self-righteous moralizers anywhere else. Essentially, there are two ways to influence human behavior, via economic incentives and via law enforcement but Boston brainiacs generally eschew both approaches.

When Boston Morons aren't telling you how fast to drive, or what type of car to drive, they will be telling you how much you should pay your nanny. Look what some idiot posted on Craigslist last week.

Paying your nanny $300 a week ?

________________________________________

Reply to: comm-158016653@craigslist.org

Date: 2006-05-06, 12:45AM EDT

is less than $10 an hour. Would you work for that? What kind of person will work for such low pay? Someone you'll regret hiring. Aren't your kids important? Being a nanny is not hanging out by the pool. I teach, take children to activities, break up sibling arguements[sic], stay late, come in early, etc. So splurge and hire the best for yourkids![sic]

Can you be a bigger loser than this dingbat?

She is going to single-handedly raise the wages of nannies everywhere - or so she thinks.

Now look at another self-evident Moron posted on Craiglist.

BE PREPARED TO RESPOND IF YOU ARE GOING TO POST

________________________________________

Reply to: sale-158847915@craigslist.org

Date: 2006-05-08, 8:25PM EDT

THOSE WHO POST ITEMS FOR SALE SHOULD BE GRACIOUS ENOUGH TO RESPOND TO THOSE OF US WHO MIGHT SHOW INTEREST IN BUYING YOUR ITEM(S). I KNOW IT CAN BE OVERWHELMING AT TIMES THE AMOUNT OF RESPONSES YOU GET, BUT OUT OF COMMON COURTESY IT IS ONLY FAIR TO RESPOND. EVEN IF IT'S JUST TO SAY YOUR ITEM(S) ARE NO LONGER AVAILABLE. US BUYERS ARE THE ONES WHO PAY YOU, THINK OF HOW YOU MIGHT FEEL!!

Idiot, I don't think one Craigslist seller's behavior will be altered your post. Hey, but why let that reality impede on your own whining self-righteousness.

And the sterotype holds that all of the moralizers are Southern rubes...

Excuse my pedantry, but I learned the word "inure" back in high school. According to Dictionary.com it means:

To habituate to something undesirable, especially by prolonged subjection; accustom: “Though the food became no more palatable, he soon became sufficiently inured to it” (John Barth).

I'll never forget that word because of how I learned it. It was used to describe Kapos, the prisoners in concentration camps who supervised, often brutally, their fellow captives. I believe I saw the word in Viktor Frankl's book.

More than a few times I have asked, rhetorically or explicitly, why the heck people live in Massachusetts. My answer has always been "inertia". They live here because they were born here. And I guess they stay here because they have been inured to the misery.

Two weeks ago I aptly described the climate up here.

Though I grew up in Massachusetts, I never realized how dour the climate was until I came back. A warm day in February will undoubtedly be spoiled by rain. If the sun is shining, count on a stiff northerly breeze. And quite frankly, the sun isn’t often out much at all. It’s almost like living in a lake effect region of upstate New York. Even in this “global warming” induced mild winter, it still snowed on October 28th. Inertia has got to be the only reason people continue to live here.

Those of you lucky, or smart, enough not to live in New England probably saw the flooding rains that hit here last weekend. It's been brutal. On Saturday I hit weather.com to see the 10-day forecast. Unbelievably it was predicting rain FOR THE NEXT 10 DAYS.

And guess what....it had already been raining for the preceding 5 days. It's mid-May, and I have only played golf up here once this year. I even had to put the heat on for a few minutes this past Sunday. My toddler son is going stir crazy because I haven't been able to take him to the playground for over a week, and counting.

Lifelong residents, like my parents, have become inured to this weather.

They have also become inured to the feckless government, moralizing fanatics, and static economy. Forbes recently ranked Boston the 200th (out of 200) cheapest city to do business in - in other words, the worst.

Since my April 26th post, the number of homes for sale in Newton, according to Realtor.com has risen from 704 to 724. I just realized that those numbers may not do justice to the currently reality because of the rapidly growing number of FISBOs (For Sale By Owner). Just at the end of my block are four FISBO signs.

I am also happy to report that two of my friends recently sold their homes sans broker - saving them tens of thousands of smackeroos.

People have always had this option, so why all of a sudden are thousands of people opting to sell their own homes?

My answer is pure contagion. Once somebody hears of another doing it, they themselves submit to the power of suggestion. Then the idea spreads virally.

The same applies to this Southern migration. Florida and Arizona have always been cheaper and warmer. So why only now are hordes migrating away from the dank and dreary Northeast?

Devil's Advocate: Isn't it pure demographics - aging Baby Boomers seeking warmer climes and lower state taxes?

Sure that is part of it, but don't try to discount my contagion theory. In Charlotte, all of the newcomers are actually young people from the Northeast. The non-Boomers, including more than a few of my friends, are moving to Florida and Arizona as well. It's one thing to be merely aware of a faraway nicer, warmer, and cheaper place to hang your hat, but quite another to know friends or family members who've already taken the plunge. Plus, in the internet age, it takes 2 seconds to click on a link and see how much house you can buy down there or perhaps to see the weather forecast in Florida.

Almost everyone I met in Charlotte was a displaced Northerner. There they are called "Yankees" by the increasingly marginalized natives. Everyone's story was the same. They followed a friend, brother, or a job down there. They had people following them - often times their own parents. (So much for that in-law buffer zone!)

I really don't know how statistically significant those 700+ homes for sale in my town really are. But my hunch tells me that real estate in Boston will languish for years to come. As jobs and young people keep moving, the tax base will continue to erode, which will lead to more and more taxation, further aggravating the exodus. Massachusetts really is in an economic death spiral.

Furthermore, in my opinion, there is nothing that can prevent this. I am bearish on the stock market, but there are potential catalysts that could turn me bullish (lower taxes, entitlement reform, etc.) If you saw a stock with no hope for profits, you wouldn't sink a penny into it. I feel the same way about real estate in Massachusetts (and California).

By the way, first time home buyers today are going to be hurt the most. Thirty year fixed mortgage rates have gone up over a point to around 6.5% and yet real estate prices haven't dropped enough to reflect that. For example, last year it would cost you $2,839 per month for a 30 year fixed mortgage (5.5%) on $500,000, yet today it would cost you $3,160 for the same loan at today's rates (6.5%).

A $300 increase in cost should roughly translate to a $50,000 decrease in price. Do you think 500k homes are 10% off of their price peak? I certainly don't.

This is what I mean about today's first time buyers getting hurt. When interest rates are factored in, real estate is actually higher priced now than ever.

Here is the stock market analogy. It is generally safer to buy a high flying stock trading at 100 times its earning estimates when it is growing rapidly, than it is to buy the same stock when it drops to 50 times its estimates but is losing earnings momentum.

The worst case scenario is playing out for real estate. Instead of a quick 20-25% correction, the market is just stagnating, staying overbought, and sucking more buyers in at these nosebleed prices. It's most certainly going to make the eventual correction more severe.

Oh yeah, about that death spiral...

41% of Massachusetts residents have recently thought about moving out of state.

No comments:

Post a Comment